Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. Finance Strategists is a leading financial education organization that connects people with financial professionals, priding itself on providing accurate and reliable financial information to millions of readers each year. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content.

Purpose of standard costs LO1

With either of these formulas, the actual quantity used refers to the actual amount of materials used to create one unit of product. The direct materials quantity variance of Blue Sky Company, as calculated above, is favorable because the actual quantity of materials used is less than the standard quantity allowed. With either of these formulas, the actual quantity used refers to the actual amount of materials used at the actual production output. The standard quantity is the expected amount of materials used at the actual production output. If there is no difference between the actual quantity used and the standard quantity, the outcome will be zero, and no variance exists.

Get in Touch With a Financial Advisor

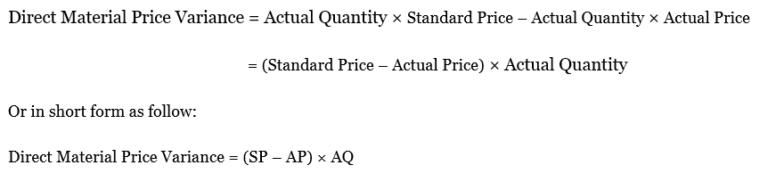

According to ABC Company’s annual budget of 120,000 production units, 360,000 units of raw material are to be used (3 units for every finished product). The total budget for raw materials is $900,000 ($2.50 per raw material). The difference between the standard cost (AQ × SP) and the actual cost (AQ × AP) gives us the material price variance amount. The direct material price variance is also known as direct material rate variance and direct material spending variance.

What is the formula to calculate material quantity variance?

Direct material price variance (DM Price Variance) is defined as the difference between the expected and actual cost incurred on purchasing direct materials. It evaluates the extent to which the standard price has been over or under applied to different units of purchase. To illustrate standard costs variance analysis for direct labor, refer to the data for NoTuggins in Exhibit 8-1 above. Each unit requires 0.25 direct labor hours at an average rate of $18 per hour for a total direct labor cost of $4.50 per unit. During the period, 45,000 direct labor hours were worked and $832,500 was paid for direct labor wages.

- Each of these variances are discussed in detail in the following sections.

- The total variances can be calculated in the last line of the top section of the template by subtracting the actual amounts from the standard amounts.

- He estimates that each unit should require 4.2 feet of flat nylon cord that costs $0.50 per foot for total direct material costs per unit of $2.10.

- At the beginning of the period, Brad projected that the standard cost to produce one unit should be $7.35.

The amount of materials used and the price paid for those materials may differ from the standard costs determined at the beginning of a period. A company can compute these materials variances and, from these calculations, can interpret the results and decide how to address these differences. This result is interpreted as the organization paid $30,000 more for materials used in production than they planned. This direct materials price variance could indicate a purchasing issue, such as the purchasing department paying more than the agreed-upon amount (purchase order amount). Or the cause could be a supplier or sourcing issue in which the material can be sourced cheaper elsewhere.

Variable manufacturing overhead efficiency variance

It could mean that the direct materials quantity standard needs to be reduced to achieve an accurate standard variable cost per unit. Or, further investigation might reveal a production error in which the units were improperly sized, which is a significant quality control issue. The total amounts for direct materials actually purchased and used are reported on the following line. The actual quantity purchased and used to produce 150,000 units was 600,000 feet of flat nylon cord costing $330,000.

Whatever the cause of this unfavorable variance, Jerry’s IceCream will likely take action to improve the cost problemidentified in the materials price variance analysis. This is why weuse the term control phase of budgeting to describevariance analysis. Through variance analysis, companies are able toidentify problem areas (material costs for Jerry’s) direct materials variance formula and consideralternatives to controlling costs in the future. Note that both approaches—the direct materials price variancecalculation and the alternative calculation—yield the sameresult. Where,SQ is the standard quantity allowed,AQ is the actual quantity of direct material used, andSP is the standard price per unit of direct material.

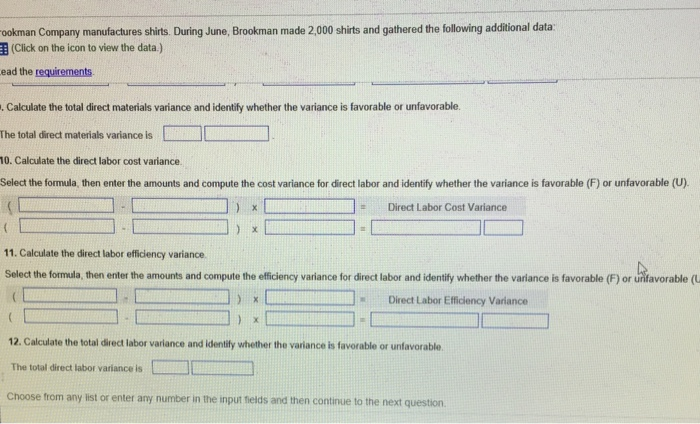

The completed top section of the template contains all the numbers needed to compute the direct labor efficiency (quantity) and direct labor rate (price) variances. The direct labor efficiency and rate variances are used to determine if the overall direct labor variance is an efficiency issue, rate issue, or both. A template to compute the total direct labor variance, direct labor efficiency variance, and direct labor rate variance is provided in Exhibit 8-6. At the beginning of the period, Brad projected that the standard cost to produce one unit should be $7.35.

Forauto suppliers that use hundreds of tons of steel each year, thishad the unexpected effect of increasing expenses and reducingprofits. For example, a major producer of automotive wheels had toreduce its annual earnings forecast by $10,000,000 to $15,000,000as a result of the increase in steel prices. Standard costs are cost targets used to make financial projections and evaluate performance. A cost formula is used to predict the expected cost for a specific expenditure. Direct materials refer to basic materials that form an integral part of a finished product. GR Spring and Stamping, Inc., asupplier of stampings to automotive companies, was generatingpretax profit margins of about 3 percent prior to the increase insteel prices.

Web Cams Sex